At its core, impact investing is about deploying capital with the intent to bring about some socially desirable outcome with the expectation of a financial return.

There are two key elements:

An Investment with the Intention to Do Good

An expectation of Financial Returns

Baked into this definition is some subjectivity. Specifically, what may be a socially desirable outcome for one person may not be the same for another.

Nonetheless, generally, the social outcomes investors seek are unlikely to face much dispute even from the most critical investors. Some of the causes impact investments often support include; lowering greenhouse gasses, eradicating poverty, increasing economic opportunity for underrepresented communities and feeding the hungry. The expectation of financial returns is significant because it is what separates impact investing from philanthropy.

What else should I factor into the definition?

In addition to the two basic elements, an intention to do good and expectation of financial returns, some institutions add a third factor, impact measurement.

The thought is if you intend to do good, you should measure how much good you’re doing. We explore measurement in more detail later.

Within these 3 elements, there’s a lot of wiggle room, often guided by individual investor’s goals and personal interests, their priority on returns vs social outcomes, and the methodology they apply to outcome measurement.

The Fluidity of the Definition of Impact Investing

Given that impact investing is a relatively new concept, its definition can vary based upon who you ask. McKinsey explains this well:

“‘Impact investing’ means different things to different people. Some see it as a strategy for beating financial benchmarks, because businesses that target unmet social or environmental needs can be profitable but easy for investors to overlook. Others are happy to accept lower financial returns for the sake of backing enterprises whose main interest is creating social benefits.”

As suggested above, impact investing can be associated with an acceptance of below-market returns. While this is certainly true for some products, many impact vehicles now work to meet or beat market returns.

How Do Industry Participants Define Impact Investing

One of the leading voices in impact investing, The Global Impact Investing Network (GIIN) defines impact investing as “Investments made into companies, organizations, and funds with the intention to generate social and environmental impact alongside a financial return.”

Michael Drexler and Abigail Noble of the World Economic Forum define impact investing as “an investment approach intentionally seeking to create both financial return and positive social impact that is actively measured.”

The Financial Times also includes measurability in its definition, “Impact investing is generally accepted to describe investing that intentionally seeks measurable social and environmental benefits.”

As you can see there are some common threads within the definition. As the industry matures, it is likely a standard definition will be accepted by all stakeholders.

How does CNote define Impact Investing?

At CNote we agree with the generally recognized definition that impact investing involves deploying capital with the aim of creating some measurable positive social outcome with the expectation of financial returns.

Where we diverge is our belief that every investment is actually “impact investment.”

Why?

Because whether or not you are targeting a social outcome when investing, your investment decisions will have consequences on society. This is because the flow of capital will incentivize or disincentivize actions by entrepreneurs and businesses on the aggregate–intentional or not, your money has an impact.

Ultimately, the important question we should ask before we make any investment is: What social outcomes does this investment support, and are those outcomes aligned with my goals and values?

The question then is one of intentionality; are you being conscious about what your money is doing and are you aligned with the outcomes it is supporting? This is extremely important knowing that even small investments in the aggregate can drastically shape industries, corporate behavior, and societal outcomes.

In recognition of the notion that every investment choice has a consequence, our hope is that in the long term, impact investing as a standalone term becomes redundant and will just be called “investing.” As impact investing matures and becomes more standardized and measurable, many of the “niche” metrics we use now to measure impact may become as essential as metrics like the Price/Earnings ratio.

Why does the definition of Impact Investing matter?

How and where you invest is important. Understanding how the industry and individual participants approach impact investing can help you ask more informed questions and ultimately make better choices for where you want to put your money to work.

Impact investing, as a movement, is still evolving and seeking standardization. It is important to understand how various industry leaders define the term and how it affects their approaches and methodologies–which can vary widely.

At CNote, we want you to make the most informed investment choices. Hopefully, this article leaves you with a better understanding of how to approach impact investing as an investment strategy.

Impact Investing Metrics and Themes

The GIIN (Global Impact Investing Network) has created Impact Reporting and Investing Standards (IRIS) metrics to provide a standardized way to compare different investment options. While the GIIN is highly regarded, there are over 500 metrics and applying and making sense of these metrics can be challenging for the unfamiliar and can be cumbersome for even experienced impact investment practitioners.

Another route towards standardization is by aligning investments with the United Nations Sustainable Development Goals (SDGs). The 17 SDGs were adopted by all 193 UN Member States as part of the 2030 Agenda for Sustainable Development. These goals are an urgent call for action to solve the world’s greatest development challenges, ranging from an end to poverty and reduced inequality to tackling climate change.

Many impact investors are now aligning their goals and investments with the SDGs. The general consensus is that they are a useful framework and common language through which we can all communicate broader sustainability efforts. It is also generally appreciated that alignment is an ongoing process with most still trying to figure out how to get it right.

As a result, there are movements by impact investors and measurement institutions to incorporate the SDGs into their impact measurement frameworks. Toniic institute has developed the SDG Impact Theme Framework and the IRIS metrics have been aligned with SDG indicators that they deemed appropriate for investment. Moreover, IRIS is launching, IRIS+, which should include a more comprehensive look at the SDGs.

Another group working on this is the Impact Management Project, a forum of 2000+ impact investing practitioners. Having just completed Phase 2 of the development process they are looking to build consensus on ‘how to measure, report, compare and improve performance.’

The complexity of these metrics highlights another issue, the approach to impact investing depends on who the investor is.

To illustrate, large institutional investors may specifically require; risk models, impact measurement audits and put in place other restrictions that a retail investor may not. Moreover, a retail investor may want to see tangible short-term outcomes; homes built or jobs created, among other metrics, whereas an institutional investor may have a longer time horizon or seek outcomes that are harder to quantify. Understanding the audience and their expectations will radically shape how one views a given impact investment.

History of Impact Investing

The term ‘Impact Investing’ was created in 2008 at meetings convened by the Rockefeller Foundation in Italy. Although the definition is relatively new, the tradition of Socially Responsible Investing (SRI) is not. Religious communities have been practicing SRI for thousands of years and it can be traced to biblical times, as outlined in Jewish and Sharia law. This SRI involved making no investment in alcohol or tobacco, which is today regarded as negative screening. United-States-based SRI can be traced back to the 18th Century to the Methodists who also employed negative screening, extending it to include gambling as well, and to the Quakers who banned investment in slavery and war.

The modern roots lie in the Vietnam and Civil Rights Movements notably with South African Apartheid and divestment from the country. In the 1990s and 2000s, this shifted from negative screens to positive screens. The term broadened and in the preceding decades impact investing as it is today was born.

Today, impact investors can be, but are not limited to; fund managers, development finance institutions, foundations, government agencies, NGOs, pension funds and insurance companies, religious institutions, and individuals. Recently there has also been a rise in the number of online impact investing platforms, like CNote, which have made impact investing widely accessible to all individuals.

Impact Investing Approaches

The existence of impact investing highlights the current paradigm shift in how the business and investment community is thinking about; place, planet, product, and processes. This shift materialized as the double bottom line approach, which is measuring performance in terms of not just financial considerations but also social impact, and triple bottom line which adds environmental impact into that discussion. This evolved into SRI, and the introduction of negative screening, and ESG which incorporates Environment, Social and Governance factors into the investment process.

Socially Responsible Investing (SRI) vs. Impact Investing

Socially responsible investing is focused on deploying investment dollars in a responsible and positive way. Typically SRI involves the use of negative screens or filters when selecting investments. Often these screens ensure that a fund avoids investing in certain things the fund manager deems undesirable like companies that produce weapons, tobacco, and oil.

In contrast, impact investing actively seeks out investments that will create a positive economic, social, or environmental impact. Another way to think about this is as “do no harm” for SRI versus “do good” for impact investing.

What about Environmental, Social and Governance (ESG) Investing?

ESG investing is about critically viewing an investment target’s environmental, social, and governance practices in the due diligence phase of investment. The key difference between ESG and impact investing is that ESG typically serves as a screen to weed out companies with unacceptable practices, whilst still prioritizing the maximization of financial returns.

For example, let’s say an institutional investor was evaluating investments in multinational clothing companies, they may view supply chain practices as a key ESG metric because they want to make sure any target companies avoid the use of child labor and ethically source their raw materials.

ESG is most commonly used in the context of public market investing, where one is evaluating the environmental, social and governance structures of a given company and evaluating whether that entity is taking sufficient steps to meet or exceed specific areas of corporate responsibility.

Some research suggests these ESG-focused investments can actually lower the riskiness of an investment. To illustrate, if you know a target company maintains an ethical supply chain, the risk of damaging headlines about child labor practices (and an associated drop in stock price) are greatly reduced.

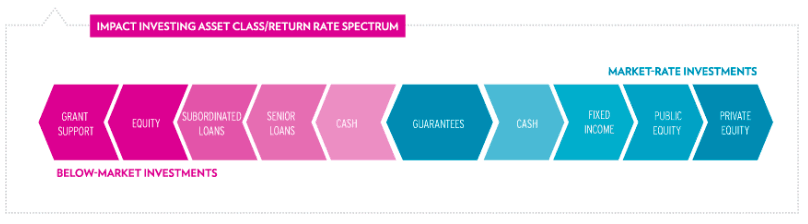

Impact Investing Across Asset Classes

Impact Investing occurs across asset classes and with a broad range of financial instruments. The main asset classes include; fixed income, real assets, public and private equity and private debt. The majority of impact investments are currently in private equity and private debt. There are ongoing discussions by many in the field about whether impact investing could emerge as its own asset class because it drives development and uses specialized metrics and benchmarks, but this is yet to be seen.

Returns will vary greatly based on the type of investment and the market size related to the social issue. While the market for improving crop yields in developing countries is likely large, both in terms of potential financial and social rewards, the same may not be true for addressing something like increasing societal interest in the arts.

What to expect for financial returns depends solely on the strategy and philosophy of the investor. Anyone considering an impact investment, or any investment would be well served to ask the fund manager or company, about what their priorities are, how they measure success, risk, and other non-investment outcomes.

How popular is Impact Investing?

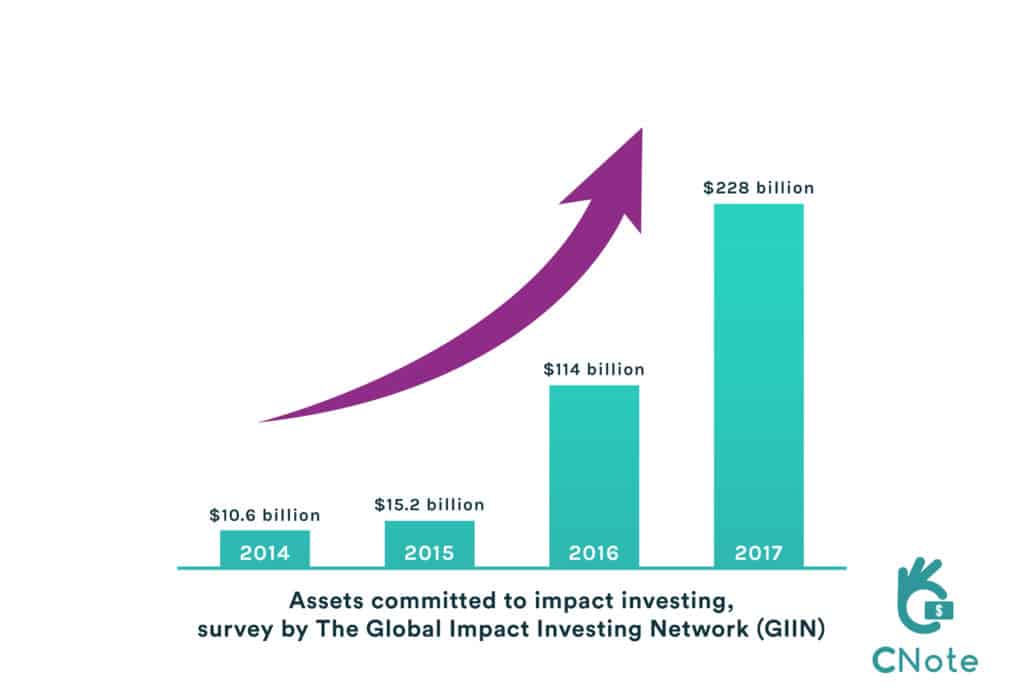

What many don’t realize is that impact investing has grown to become a serious force in the investment world which dictates the flow of billions of dollars in capital each year. In 2017, according to GIIN’s Annual Impact Investor Survey of 225 companies, the total amount invested in impact funds was at least $114 billion. This is up from 2015 and 2016 when the impact investing market totaled $7.1 billion and $15.2 billion, respectively.

Financial giants like Goldman Sachs and Zurich Insurance are now earmarking $13.7 billion toward impact investing. BlackRock, the world’s biggest asset manager, has created a division solely devoted to impact investments. There is also attention from international organizations like the UN which has gathered over $62 trillion USD from more than 1,500 asset managers to fund the Principles for Responsible Investment.

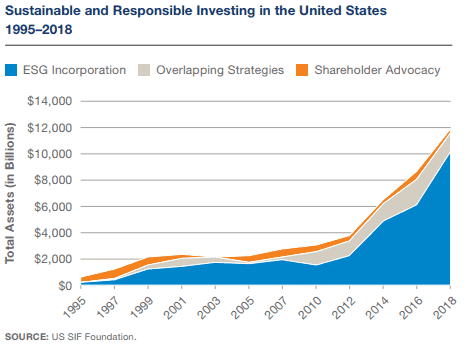

While the chart above only reflects those surveyed by the GIIN, the chart below from the US SIF: The Forum for Sustainable and Responsible Investment, shows that over $12 trillion in assets have been deployed across ESG, SRI and other impact-focused strategies as of 2018.

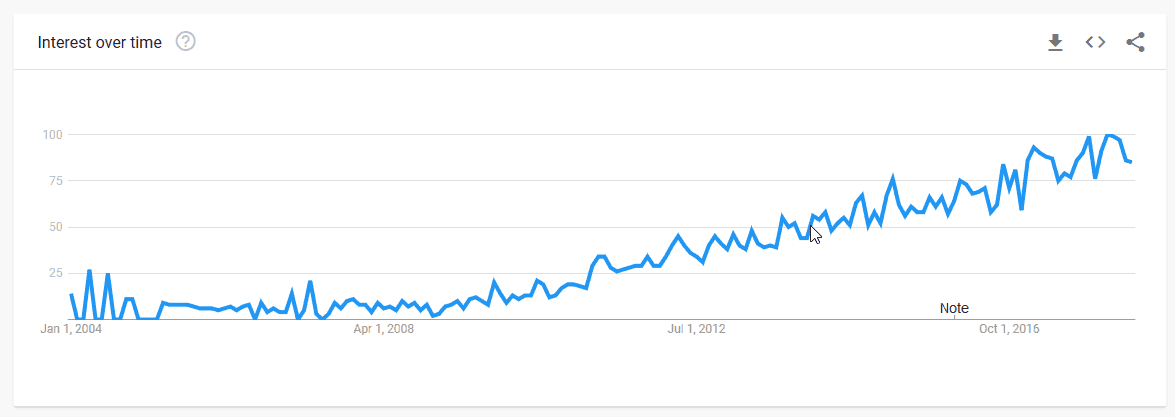

Established institutions aren’t the only ones interested in impact investing. Since 2008, Google search reports for “impact investing” have increased significantly. The trend does not show any likelihood of tapering.

In a recent survey of over 1,300 financial advisors and analysts, the CFA Institute found over 50% considered ESG integration a major priority and were taking steps to include it in their analysis.

Moreover, the world is about to see a massive transfer of wealth from baby boomers to millennials. By 2020, millennials will have an estimated cumulative wealth of $24 trillion, and surveys show a whopping 76% of them believe how they invest can have an impact on responsible investing. Further studies show that millennials are 2x more likely than the average investor to invest in companies with social or environmental goals. Explore more statistics indicating the rising trend at Morgan Stanley.

Why Impact Investing?

Here are just a few reasons to impact invest. This list is not exhaustive, and what moves one investor may ring hollow for another.

Align your investments and your values – because impact investing does good and generates financial returns, investors can support the causes they care about whilst putting their capital to work.

Increase Portfolio Stability – A Morgan Stanleystudy, of over 10,000 equity mutual funds over 7 years, found that, on average, impact investing funds had lower volatility than comparable non-impact funds.

Expand your network – The impact investing community includes ppolicymakers entrepreneurs, human rights activists, and development experts, all dedicated to utilizing capital in pursuit of tackling important societal issues.

Critiques of Impact Investing

The world of impact investing is not without faults. Like any booming industry, there are those who would co-opt the concept for profit. Impact investing is having a golden moment of rapid growth and popular support and, according to Business Wire, is expected to grow to $307 billion by 2020 (2x what it was in 2017). As a result, some investment vehicles ostensibly use the “impact investing” label without actually committing to the underlying strategy, in an effort to attract investors.

Sometimes this is referred to as ‘greenwashing’. In the impact investing industry, there are many that are concerned that mainstream asset managers are increasingly promoting and marketing ‘impact strategies’ without sufficient evidence that they are following through with these claims, measuring and reporting towards them. Unfortunately, this means that impact investors must carefully review investment documents and scrutinize impact measurement practices to assure that the product they are investing in accomplishes what it claims to do.

Another potential pitfall of impact investing is a lack of understanding or analytical rigor around quantifying the effect an investment has on a specific issue (like affordable housing). For example, with microloans, lenders track number of borrowers, repayment rate, and business growth. However, knowing this information doesn’t necessarily capture the true impact, or what that community would look like without its microloans. In some instances, measurement may be too difficult given a myriad of variables, in other cases, it may simply be impossible to fairly measure a given investment’s impact.

Another popular critique is that impact investing is skewed towards the wealthy and, by allowing for positive social impact and market-rate returns, keeps the concentration of wealth with the already well-off.

Conclusion

Whether you actively seek to align your dollars with your values, it’s clear that impact investment is rapidly growing and is changing the status quo of capital allocation. Traditionally, funding and loans were only available to people with great credit or leverageable assets. Impact investing changes this dynamic by looking beyond financials and seeing whether your investment will generate positive social returns, not just financial ones. Ultimately, impact investing breaks down the perceived wall that exists between capitalism and social good. We can have our cake and eat it, too.

Let us know what you think about this piece! What information do you wish we included or what questions do you still have? Email hello@mycnote.com

Additional Reading

There is an ever-growing library of resources for learning more about impact investing on the web. Here are some good resources if you’re looking to dive deeper on impact investing

The GIIN site includes resources for continued learning about impact investing, including case studies and research: https://thegiin.org/

CNote Launches Wisdom Fund to Close Lending Gap for Women

New impact investment vehicle provides funding to underserved women of color and low-income women entrepreneurs across the country

OAKLAND, Calif., March 20, 2019 — Women are the fastest-growing group of entrepreneurs in the U.S. Yet less than 5 percent of small business lending—only $1 in $23—goes to women. CNote aims to fix this disparity with the Wisdom Fund, a new impact investment opportunity launching today.

Created in partnership with mission-driven lender CDC Small Business Finance and four innovative nonprofits, the Wisdom Fund funnels money from accredited investors—institutions, funds, foundations, family offices and individuals—into business loans for low- to moderate-income women and women of color. The loans are provided by nonprofit community lenders with decades of experience delivering the capital and resources that women small business owners need.

Fixing a social injustice

“We hear a lot about the gap in venture capital funding for women, but the vast majority of women who need capital are not forming hyper-growth startups; they are starting small businesses to pursue economic freedom, flexibility and independence. The financial system is not serving them well, and we’re very much failing women of color in particular,” said Catherine Berman, CEO and co-founder of CNote, an impact investing platform whose mission is to close the wealth gap in the U.S.

“With the Wisdom Fund, we’re taking a major step toward fixing a huge injustice—women’s businesses receive far less funding than they deserve,” said Berman. “We’re working with an amazing group of nonprofit community lenders nationally to entirely rethink lending to women.”

CNote is also already earning support from major corporations as well as nonprofits. “Access to capital is one of the top challenges female small business owners face and we’re excited to see CNote working to combat this with the introduction of their Wisdom Fund collaboration,” said Amy Neale, vice president and startup engagement lead for Mastercard Start Path, which supports high-potential startups around the world, including CNote. “At Start Path, we look forward to helping CNote scale their business to ensure a more inclusive economy, because when you invest in women the returns are priceless.”

Collaboration drives scalability and impact

During a three-phase build-up, Wisdom Fund partners will collect, share and act on data about what works for women entrepreneurs. In the first eight months, participants will fill in the knowledge gap, gathering information on how women interact with the loan process, what hangs them up and what eases their path. In phase two, the partners will experiment with new ways to serve women that remove barriers. Around the one-year mark, the focus will shift to scaling the program by continuing to add new lending partners, increasing investment and implementing best practices across the network.

“There’s lots of data on how women are shut out of venture capital. We don’t know as much about why women are shut out of debt capital,” said Allison Kelly, senior vice president of strategy and innovation at CDC Small Business Finance. “What are the product-level needs? Who are the business owners and what barriers are they experiencing? Why are women opting out of taking on debt? The whole financial system is set up to serve a certain segment of the population. Maybe we need to rethink the distribution of capital and how we assess risk. The Wisdom Fund is an opportunity to create new debt products by working collaboratively with the women we aim to serve.”

CDFIs are an under-the-radar impact powerhouse

Community development financial institutions (CDFIs) like the ones CNote is working with are perfectly positioned to take on this work. They’re distributed across the country, they have always invested in financially underserved communities, and they have enormous unrealized potential for financial and impact returns.

“We looked at the trends and realized that CDFIs are undercapitalized,” said Kelly. “The sources of capital were mismatched to CDFI needs—it was all big capital sources deploying larger chunks of capital to fewer and fewer CDFIs.”

That’s where CNote comes in. Since its September 2017 debut with a product for retail investors, the fintech startup has invested more than $18 million in underserved communities through a growing CDFI network covering more than 35 states. Those investments have helped to create or maintain over 2,000 jobs and fund more than 400 small business loans.

Investors can start funding women-owned businesses now

Investors in the Wisdom Fund will earn an estimated 1 percent annual return, over a 60-month term, on a loan portfolio that’s diversified across established CDFIs. Email info@mycnote.com to learn how you can help fund more women-owned businesses today.

Women seeking loans should contact a participating CDFI. Partners in the Wisdom Fund’s first phase include:

Carolina Small Business Development Fund, which provides small business loans and financial training to startups, existing businesses and community organizations in North Carolina.

LiftFund, a Texas-based organization that empowers underserved entrepreneurs with capital and support services in 13 states.

TruFund, a national nonprofit organization that provides affordable capital and business development services to small businesses and nonprofits in Alabama, Louisiana and New York.

In addition, Pacific Community Ventures will match all borrowers from the Wisdom Fund with pro bono business advisors. Pacific Community Ventures, a Bay Area–based CDFI, invests in small businesses in California that are past the startup phase and creating jobs, and manages a national network of pro bono expert advisors who mentor small business owners on any topic, challenge, or opportunity.

About CNote

CNote is an award-winning, first-of-its-kind financial platform that allows anyone to make money investing in causes and communities they care about. With the mission of closing the wealth gap, CNote directs every dollar invested toward funding female- and minority-led small businesses, affordable housing and economic development in financially underserved communities across America.

About CDC Small Business Finance

CDC Small Business Finance is a leading small business lender, award-winning nonprofit and advocate for entrepreneurs. Over four decades, it has provided more than $18 billion in funding to over 11,000 borrowers…and counting. Its lending also plays a role in bolstering economic development, and has helped to create or preserve more than 200,000 jobs in California, Arizona and Nevada.

The presenters highlighted some of the investment options currently available, tools for measuring impact, and some unique advantages that come with an impact investment strategy.

CNote’s CEO, Catherine Berman, presented for CNote and answered attendee questions about CNote’s offerings and how CNote is helping to mobilize more community investment.

The webinar is worth a listen if you’d like to learn more about impact investing.

Webinar Recording and Slides

If you weren’t able to watch the webinar live you can watch the recording at your leisure. You can also download and review the slides here.

Join CNote’s Mailing List To Get Updates About Future Webinars

If you’d like to stay in touch and get notifications when we host future webinars and other events, please provide your email below.

[et_bloom_inline optin_id=”optin_4″]

Financial Professional Looking For More Information?

If you’re a financial advisor looking to offer CNote to your clients, visit our Advisor page to learn more about how CNote can help you deliver strong returns and impact to your clients. There, you can also start a conversation with one of advisor onboarding experts.

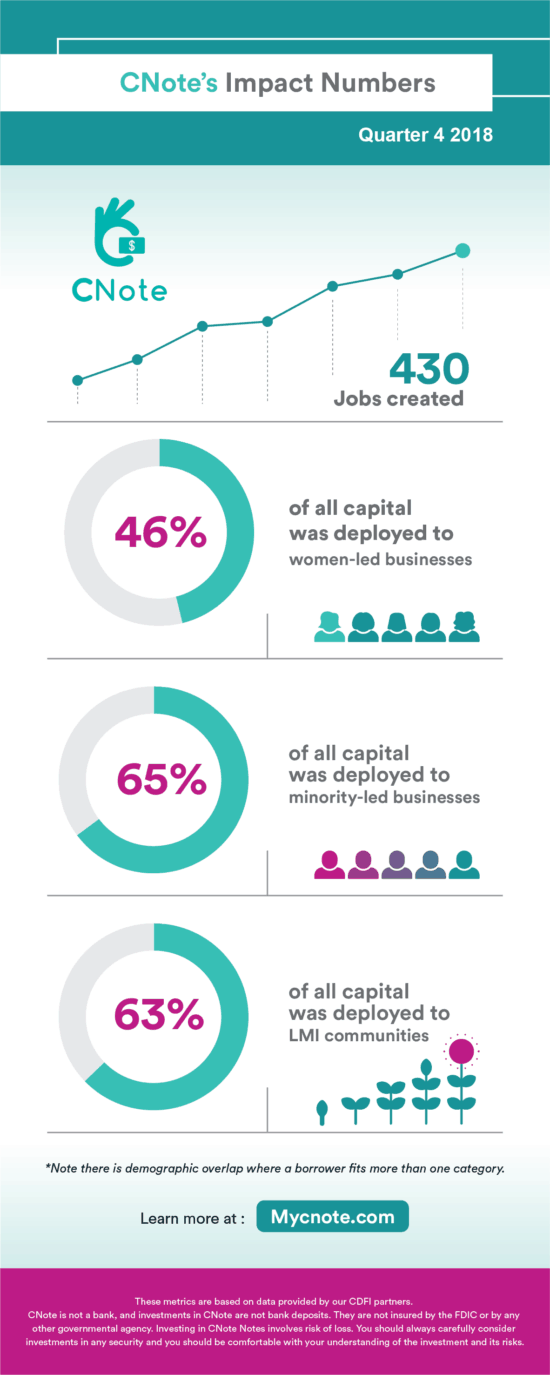

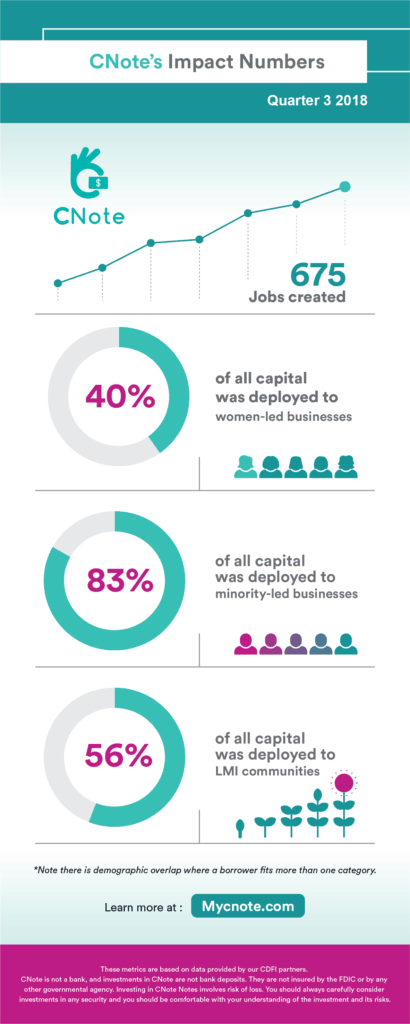

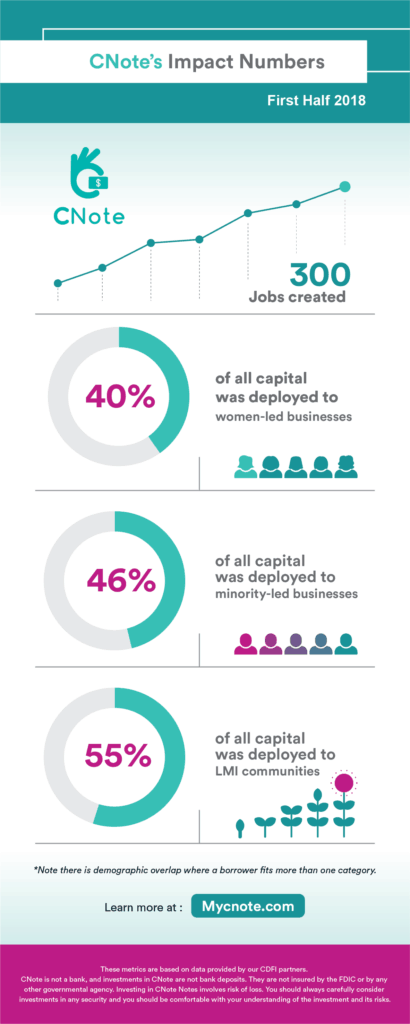

As you may have noticed, our quarterly job creation numbers are trending upwards along with our allocations across key demographics, like women, minority communities, and LMI communities.

In Q4 2018, our members helped create/maintain 430 jobs!

Over 65% of all invested capital was deployed with minority-led businesses!

We are extremely proud of our Q4 results and will be releasing our full 2018 Impact Report shortly. In the interim, check out our 2017 Annual report.

That idea is embedded in our social mission of closing the wealth gap and building a more inclusive economy for everyone.

Our team thought it was only natural we formalize that commitment by becoming a Certified B Corporation®. Now CNote’s commitment to profit with purpose becomes even more clear for our investors, members, and partners.

We’re excited to join a growing list of companies that are working to build sustainable businesses along with a better world.

B Corps were 65 percent more likely to survive the great recession in 2009

What B Corp Status Means

CNote was certified by the non-profit B Lab to meet rigorous standards of social and environmental performance, accountability, and transparency. That required us to evaluate how our practices impact our employees, our community, the environment, and our customers.

“Think of it this way: USDA certifies organic foods, and Good Housekeeping puts its seal of approval on quality products, like washing machines and skillets. And since 2006, a nonprofit organization called B Lab has been certifying corporations it deems to be concerned about their communities and the environment.” – NPR

Certified B Corporations® are a new kind of business that balances purpose and profit.

They are legally required to consider the impact of their decisions on their workers, customers, suppliers, community, and the environment.

This is a community of leaders, driving a global movement of people using business as a force for good.

The entire CNote teams is excited to be a part of this movement!

Join us on Wednesday, Feb. 27, 2019, featuring leaders in income and impact — Cat Berman, CEO of CNote; R. Paul Herman, CEO of HIP Investor; and Sonya Dreizler, CEO of Solutions with Sonya.

The webinar will be emceed by Sonya Dreizler, who helps advisors and financial experts pursue impact Investing, and how to better manage your RIA, Mutual Fund, and Broker-Dealer.

Please join us for an insightful exploration and deep discussion on Income + Impact, along with active Q and A along the way.

What We’ll Cover

This and much more:

Portfolio options that generate Income and Impact across multiple asset classes, including strategies involving muni bonds, real estate, cash alternatives, and other asset classes

How you can invest in community development and increase capital access for women and people of color

How to structure a portfolio to target UN Sustainable Development Goals (UN SDGs) across both U.S. and Global markets

When

Feb 27, 2019, at 1:00 PM in Pacific Time (US and Canada)

A tie can say a lot about its wearer. The first ties marked out the court members of Louis XIII, a French king who had admired the neck accessories of the Croatian mercenaries and adapted them as mandatory attire for royal gatherings.1

In the following 300 years, ties evolved into the more simple and streamlined form we know of today, but through subtleties in color and pattern they continue to provide distinction to their wearer. A red tie, for instance, can signal charisma or authority, while a tie covered with hotdogs might send a different message altogether.

Product offerings at Knotty Tie Co. in Denver, CO

That said, a tie is an accessory you want to get just right. Knotty Tie Co. makes it easy to do just that.

From its chic and accessible e-commerce site, customers can select and order ties from the comfort of their own homes. With over 350 patterns and 560 color options, they can design just the right tie, bowtie, or scarf for any occasion: from themed wedding attire to workplace swag, to a thoughtful gift for a loved one. They can even customize from scratch, entering their ideas on the website, which the company’s graphic designers will then mock up for them.

It’s a unique company that creates unique ties. But even more distinctive is the story behind it.

A unique business model derived from an altruistic mission

When we asked what he did to make his customers happy, President and CEO Jeremy Priest mentioned the phrase Made in America.

“For us, Made in America isn’t just a reason to buy…”

What this means is that his company produces every tie in their facilities in Denver, Colorado. With equipment they bought and painstakingly learned how to operate, they print the patterns customers select onto quality fabric. Then they sew the fabric into ties — completely by hand.

Employee operating textile cutting machine at Knotty Tie

This allows them to produce small batches of customized ties in a relatively short amount of time, something their competitors, many of whom manufacture overseas, cannot deliver on.

“For us, Made in America isn’t just a reason to buy, it legitimately gives us a competitive advantage,” said Jeremy. Later he added, “It’s incredible how the mission [of the company] weaves into that.”

And it’s the mission of Knotty Tie Co. that truly makes it stand out. Surprisingly, it has less to do with customized ties, and more to do with the people who make them. The employees who sew the final product by hand are all refugees who fled various conflict countries to start a new life in the US.

Refugee employees at Knotty Tie

And CEO Jeremy Priest’s mission is to provide them, and other refugees, with meaningful employment opportunities.

The birth of a mission

“The mission of the company is to create meaningful employment opportunities for refugees…”

Like most people, Jeremy didn’t initially enter adult life with enough belief in a cause to build an entire company around it. Instead, his convictions grew gradually through life experiences.

The first of these was a military career of six years, four of which were overseas. “One of the things I witnessed in my military duties…was that people were yearning for economic inclusion and economic opportunities.”

Inside the store of Knotty Tie Co.

This inspired him to study economics and get an MBA in entrepreneurship. At the same time he was pursuing his studies, he saw that there was a population with economic need in his very own community: the 2,000 refugees who set roots down in Colorado each year.

“I really recognized that there were enormous barriers to employment and that society generically wasn’t really recognizing the barriers, and wasn’t recognizing the dignity of the arriving population and the contributions they could make,” Jeremy said.

One of Knotty Tie’s employees intent upon his work

Instead, many refugees had to take random jobs with odd hours as they struggled to transition to their new lives.

Thankfully, there were non-profit programs that helped refugees transition, providing English classes and developing their job skills. Jeremy volunteered for one of those programs. But a key interaction in 2011 convinced him his clients needed something more.

“To me it seemed like there was just something missing…”

He was training two refugees in janitorial skills when they told him they had 20 years’ experience in sewing and a lifetime of experience in farming. In “a crisis of his conscience,” he realized he was training them in the wrong skills.

“I appreciated the resettlement agencies…But to me it seemed like there was just something missing — and that was the connection between [the refugees’] existing skills and the employment pathways we should be putting them in touch with.” And that made it less meaningful for them.

Employee cutting tie

Thus began an effort to convince the non-profit to not only train the refugees in basics, but employ them in their existing skills, namely sewing. But when Jeremy realized this was outside the scope of the program, he began to take matters into his own hands.

Scrapping it

Raising up his own enterprise to employ refugees in meaningful work was no easy task. In the beginning, it was just Jeremy and his undergrad classmate and co-founder Mark — and they had to scrap it.

Knotty Tie co-founders Mark Johnson and Jeremy Priest

“Truth be told Mark and I were just so broke that we didn’t have cars,” Jeremy told us when talking about the early days of his company.

“Our first office was in an artist collective and we had to be able to walk there.” During their Kickstarter campaign in 2013, the two frantically produced ties, Mark in the afternoon after his shift at a cafe, and Jeremy all day before his night classes.

As the company took shape, they sought investors who would fund them despite them not having a high credit score. Thankfully an impact investor gave them seed funding of $40,000, and with it the valuable affirmation that their idea was worth all those long hours. This enabled them to hire two refugees with sewing experience and purchase some equipment to scale their efforts. It also qualified them to receive a loan of $10,000 from Colorado Enterprise Fund, a CDFI in CNote’s network.

“CEF was really an angel at the time in which nobody one else was willing to consider us on paper…”

With the money, Jeremy and Mark were able to meet payroll and purchase more equipment.

Later, when Jeremy showed CEF they could cut costs by two-thirds by manufacturing in-house, they provided a second loan of $100,000 to buy their own textile machinery. It was through CEF that Knotty Tie was able to fully implement its Made in America business model.

Knotty Tie’s textile printing machine

“CEF was really an angel at the time in which nobody one else was willing to consider us on paper,” Jeremy reflected. “They were willing to altruistically evaluate why we’re doing what we’re doing and what we were able to accomplish to date.”

Meanwhile, Mark, who was talented in technology, had taught himself graphic design and e-commerce and taken classes in full-stack web development, all of which equipped him to make the beautiful storefront website we see today.

Future plans for Knotty Tie

Mark and Jeremy in front of their storefront

With his signature eloquence, Jeremy told us of his future plans. His vision–both lofty and inspiring–includes developing business models to employ refugees even in camps overseas.

“These are refugees, but they are self-sufficient.”

In general, he wants to spread his mission of refugee employment to other for-profit enterprises, changing the global narrative from refugees who are helpless, to “These are refugees, but they are self-sufficient.”

But for now, he is focusing on the tie company, which he hopes to make a shining example of refugee resettlement enterprises to the world.

Marc Munyakabuga, production manager

We think he’s doing a good job of it. To date, Knotty Tie has a formal board of manufacturers consisting of seven members. Additionally, it employs six sewing refugees, two of whom have started college courses to pursue careers in fashion design.

One Congolese refugee named Marc currently serves on the board as production manager. In the future, he wants to start his own small business.

Learn More:

The Colorado Enterprise Fund, was founded in 1976 and is a non-profit lending institution that offers loans to entrepreneurs and small businesses unable to get traditional bank financing. For over 40 years, Colorado Enterprise Fund has been helping people realize their dreams of starting and growing their own businesses.

CNote – Interested in helping create another success story? CNote makes it easy to invest in great CDFIs like the CEF The Colorado Enterprise Fund, helping you earn more while having a positive impact on businesses and communities across America.

Our mission at CNote is to create competitive financial products that make money for our investors while building a more inclusive economy.

Seriously.

We know its a big goal, but big goals can create big change.

Some Exciting News

Occasionally, we’re lucky enough to receive industry recognition or build partnerships that help push us towards our goals and remind us that the work we’re doing resonates with a broader audience.

This week is one of those weeks for our team.

We wanted to briefly mention a few highlights we’re proud of.

It’s a long-running program with a track record of helping startups build key partnerships and gain broader access to customers, investors, and ecosystems.

Nearly 200 companies have participated in the program, and we’ve connected with nearly 10,000 of the world’s smartest startup founders to build the future of commerce together.

Thanks to the entire Mastercard team for their support!

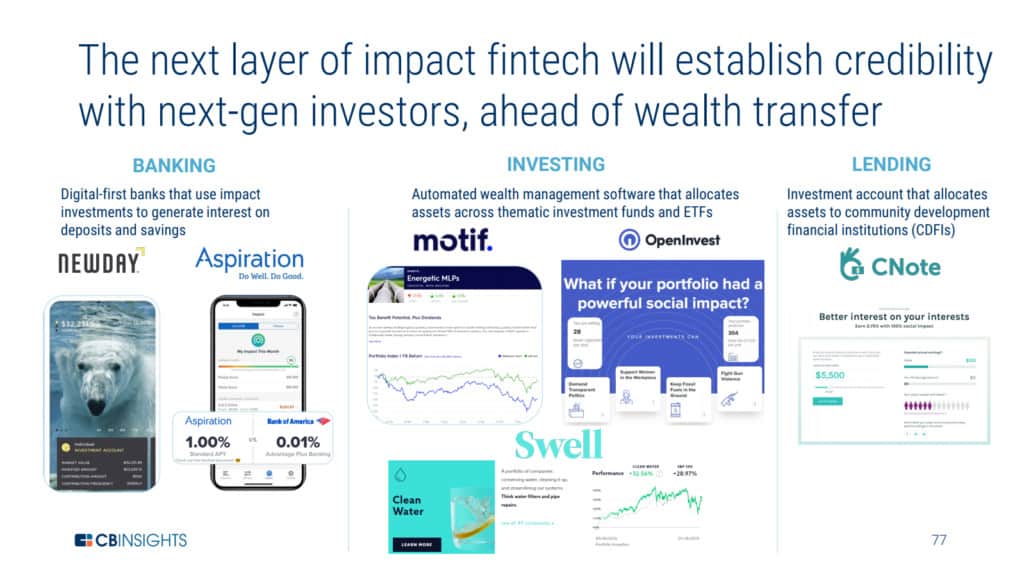

We were previously invited to their Demo Day event, and given CB Insights’ growing reputation as a key provider of business intelligence and predictor of trends, we’re grateful they think our impact-focused Fintech company is worth a mention.

If you’re interested in Fintech or just enjoy lots of charts, their 2019 report is worth a look. The slide (p. 77) mentioning CNote is excerpted below.

Credit: cbinsights.com

We’re hoping 2019 is filled with even more milestones like this. Learn more about CNote.

It’s October 1st, 2013, opening day for Nail Glam Studio and Yahaira Caraballo is nervous. After months of grueling effort, her south Bronx-based nail salon is finally ready and open to the public.

The only problem? The public didn’t come. Not on the first day, at least.

Like everything that brought her to this point, however, Yahaira’s persistence soon paid off. Although Nail Glam Studio, in her own words “didn’t make a dime the first day,” it did manage to turn a profit by the end of the first week and has only grown since.

Nail Glam Studio Founder, Yahaira Caraballo

While Yahaira’s determination enabled her to push past a number of obstacles, it took the help of many other hands to effectively turn Nail Glam Studios from a vision in her head into a thriving business.

One primary source assistance came from CNote’s CDFI partner, the Pursuit Lending, which provided essential guidance in the early stages of forming the business, along with the funds to make the necessary upgrades to comply with new regulations and to expand operations.

The other essential ingredient in Yahaira’s small business success story is family. From her brother helping to build and repair the shop to her husband providing the painting expertise, she was not short on support from those closest to her.

Yahaira did not just receive help from family, however, but was able to provide something even more important to her sister, Onaney Caraballo. In fact, one could say that Onaney was the driving force behind the idea to open Nail Glam Studios all along.

The Origins of Nail Glam Studio

Yahaira was sure that she wanted to start a business since she was young but just couldn’t find a place where she could make an impact. Despite taking on a full-time job in New York City, she still never lost her entrepreneurial ambition and continued to look for ideas and ways that she could turn her dream into reality. In the end, her sister provided the inspiration to finally take the steps towards forming a small business of her own.

Nail Glam Studio Team

Following a move to New York City from their native Dominican Republic in 2003, Onaney quickly established herself as a stylist, gaining recognition at local nail salons and practicing on Yahaira in her spare time. Seeing her sister’s talent and looking to finally realize her own dream to be a small business owner, Yahaira cleared her savings account and began to take the steps necessary to open Nail Glam Studios.

Nail Glam Studios soon become more than just a business for the two sisters. In fact, it became a way for both to live out their respective dreams and come together in a way they never previously imagined. Where Yahaira could fulfill her ambition of owning and operating a small business, Onaney could finally have the kind of stable and supportive working environment that enabled her to focus on improving her craft without worrying about working hours or other issues that usually come with freelance and studio work.

The idea was in place. Now Yahaira just needed funding to get Nail Glam Studios off the ground.

Getting a Loan

Yahaira first sought to get a personal loan from Chase Bank. Such loans come attached with high interest rates on repayment, but Yahaira was dedicated to seeing the idea of opening a nail salon for her sister through to completion. While she was refused for the loan on the grounds because that local branch did not invest in small businesses of Nail Glam’s size, she was given referrals that culminated with her collaboration with Pursuit.

Pursuit helped connect Yahaira with the right experts, who were able to walk her through the intricacies of operating a small business. For example, they taught her how to complete the required paperwork, including a fully-formed business plan, that were required to apply for a loan. Along with the business advice and guidance, Pursuit provided the loan necessary for Nail Glam Studio to comply with the aforementioned state regulations, as well as enable the hiring of two additional staff members to expand the business with new pedicure and manicure stations.

Success and Community-Centered Growth

Since that first day without a paying customer, Yahaira estimates that they see more than one new customer every day simply through word-of-mouth. She credits this to a number of factors, including her focus on providing quality service at an affordable price. However, the emphasis on building a strong community is what really sets Nail Glam Studios apart from other nail salons in the area.

To that end, Nail Glam Studios holds community events every three months, usually corresponding with public holidays like Mother’s Day and Thanksgiving. Yahaira sees the events as a way to give back to those who are a vital component in the nail salon’s success.

Yahaira particularly enjoys Customer Appreciation Month, held every October to commemorate Nail Glam Studio’s founding–and that first nerve-wracking day–where she provides free goodie bags filled with nail-care products to customers.

A Family Success

Yahaira with her brother and sister

While building a community of happy customers in the south Bronx makes Yahaira proud, the most meaningful impact comes from much closer to home. A great example coming in the form of a text message from her nephew. In that message, he thanked his aunt for providing a place for his mom, Onaney, to practice nail styling and pursue her passion. This display of gratitude touched Yahaira and served as proof that she had achieved in what she set out to do–both professionally and personally. After all, none of this would have happened without Onaney, and now the sisters have succeeded in building a thriving business together.

Looking Forward

What began as a three-person operation has, with the help of the SBA micro-loan from Pursuit, now expanded to a staff of seven. For her part, Yahaira says that she is grateful for the loan and all support she has received until now from Pursuit. “I’m speechless with everything I’ve gotten as result of submitting this application. They have a lot to offer.”

Yahaira is now paying forward the help she was given by Pursuit in her own way, assisting other small business owners in the south Bronx as they seek to overcome the inevitable struggles encountered while striving to their own entrepreneurial dreams. She also has ambitions to open another store in the future to create even more employment in the local community.

Her story underscores the commitment of CNote and the Pursuit to helping ambitious women like Yahaira receive the support they need to turn their dreams into reality and enable local communities to thrive as a result. If you, too, would like to make a difference, please consider investing in CNote today.

Pursuit – A leading CDFI based out of New York and the CNote partner that provided the loan and technical assistance that helped make Nail Glam Studio a reality

CNote – Interested in helping create another success story? CNote makes it easy to invest in great CDFIs like the Pursuit, helping you earn more while having a positive impact on businesses and communities across America.

(And Why You Shouldn’t Take Financial Advice from Twitter)

The face behind most of the financial advice you’re reading online.

Today we’re going to have a bit of fun looking at the highs and lows of financial advice available on the internet.

Don’t take this post too seriously, but nonetheless, we’ve actually tried to include some useful resources along with clearly useless advice you’ll see below.

The Bad

What happens when roughly eighty percent of people in a country have access to the internet but as many as two-thirds of them cannot pass a basic financial literacy test?

Tweets like this:

If I had a million dollars I’d invest it all in penny stocks

As we’ve grown more accustomed to having approximately the sum total of all human knowledge one click away, it is tempting to set aside rational thought and expect the top Google search results or social media will provide us the definitive answer on a topic.

While this works fine when learning innovative origami techniques or the perfect method to boil eggs, talk is cheap and uncritically trusting unsolicited online advice can be hazardous to your financial health.

For instance, you might encounter reasonable-looking money management advice like the following:

12-15% of each check should go into savings & Buy a (at least) $500 CD at your bank.

But with 6-month CD rates hovering around one percent, this means locking $500 into a CD would roughly earn a whopping… drumroll, please… $5. And even that is on the better end of what you could reasonably have expected over the past decade in what has been a uniquely low-interest-rate environment. Not bad advice, just maybe not the best advice for your situation.

Believe it or not, there are actually a lot of places to find great advice. You just have to know where to look and make sure that its a trusted source. Generally, let common sense be your guide.

One great crowd-sourced option is the Personal Finance subreddit. Not only does this community curate some of the best topical financial advice, but the admins and active users have created a great “wiki” page that answers many common financial questions and provides life-stage financial advice based on your age (25-35 example).

They also cover the fundamentals in a comprehensive way, from things like building an emergency fund, prioritizing the debts you pay off, and 401k matching suggestions (hint, contribute the % your employer will match, at a minimum).

This really basic flowchart from that subreddit provides some key guideposts on building savings and retirement investments for someone who has no idea about money:

Finally, r/personalfinance has a great reading list that can help you get started on a lifetime of financial success.

Even Twitter has the occasional gem, you just have to dig through all the junk.

If I can’t afford three, I cannot afford one. My mom would make me tell her the price of something was three times more expensive to make sure I was comfortable spending that amount. & never give into impulse buying. Think things through, if you really want it it’ll be there.

All fun aside, here are a few key qualities that distinguish the most helpful online financial advice from the not-so-helpful.

All of these criteria do not necessarily make a piece of advice useful, but you should look for at least one or two to be present before taking what you’re reading seriously.

Helpful financial advice should be:

1) Accessible

What good is financial advice if you can’t actually use it?

The most useful financial advice will be relevant to your situation and actionable. You also might ask yourself whether your financial goals match the advice on offer. If not, pay extra heed not to get sucked into an overblown get-rich-quick scheme, possibly in the form of unsolicited email newsletters alerting you to the “investing opportunity of a lifetime” in some “little-known industry” poised for “incredible gains.” If nothing else, at least such emails give us an opportunity to be thankful for spam filters.

On a positive note, there are a number of blogs that are excellent sources of accessible financial advice on topics ranging from paying off debt to building credit to first time home buying. Some examples include Money Under 30, Get Rich Slowly, and Debt Roundup, just to name a few, but you should search for the resources that best cover your particular financial needs. Just look for clear writing, up-to-date information, and a set of concrete steps that you can take to follow.

2) Authoritative

As with anything in life, it’s nice to know that advice is coming from someone who knows what they’re talking about. For instance, if you have the (ill-advised) aim to get your financial inspiration from Twitter, the odds are more in your favor if you follow the advice of Mark Cuban rather than @catluvr411invest. This doesn’t mean that celebrity investors like Cuban are always right or that anonymous Twitter users are always wrong, but it’s best not to put too much stock in the musings of strangers with little in the way of credibility.

On the topic of Twitter, there are actually some top-notch accounts run by finance experts like Meb Faber and Roger Ma that are accessible to everyone. However, Twitter is generally regarded as a good way to follow real-time financial news rather than a platform to receive actionable financial advice.

It’s important to know who’s giving you the advice.

If you like to know that the financial advice you receive is from someone who has actual qualifications on the subject, you can search the CFP or FINRA databases to check the credentials of the financial professional in question. There are also specialty websites such as Brightscope that can help you quickly and effectively find the financial planning advice you are looking for.

3) Well-Sourced

Good sources of financial advice will provide plenty of links to support any claims made, encouraging you to do your own independent research. This also signals increased credibility, although make sure you actually click the links to verify the information presented.

Creditability is especially welcome when dealing with crowdsourced platforms. For example, the personal finance subreddit mentioned above includes valuable resources and recommendations on commonly-searched topics such as budgeting and saving for retirement, even if the posters have little in the way of proven qualifications–the fact that hundreds, if not thousands of people have critiqued and reviewed the advice means its likely to be more reliable. Nonetheless, it still pays to be wary of any given forum post or comment, but there is no denying that there are occasionally some user-created gems like this personal income spending flowchart.

Conclusion

While the above tips are hardly exhaustive, sources that contain some combination of accessibility, authority and verifiability are much more likely to help you find high-quality financial advice that you are looking for.

Information on the internet can serve as a great compass or a ticking time-bomb depending on who is giving it. Clearly defining your goals in advance and bringing a measure of critical awareness to bear is key when searching for and choosing to follow online financial advice.

After all, there’s plenty of good financial advice out there on the web for those who know how to look.

In the end, the best advice is to build a foundation of personal knowledge so you can make well informed and independent decisions.

Some of y’all are getting big mad like I’m Suzy Orman & I’m supposed to be the finance Oracle. Bruh, I answered a question. Take a financial literacy class, diversify your money, & keep it gangsta pic.twitter.com/TFC0Qp1qa7

2018 was a time of significant growth for CNote. The total number of users on our platform grew substantially and we took on institutional investments from amazing partners like the Sierra Club Foundation.

This influx of capital meant we were able to deploy more assets to our network of non-profit lenders across America. Those CNote-investment dollars funded loans that helped individuals pursue their dreams of starting small businesses, helped build affordable housing, and helped to bring economic development to communities that need it most.

Our intention is to continue to deliver competitive financial returns while generating measurable and significant positive social impact. To that end, we’ve roughly doubled our impact metrics from 2017, across the board. While pleased with the 800 jobs created/maintained in 2017, we are thrilled that we nearly doubled that number to more than 1,400 in 2018.

Additionally, our growing network of partners that now covers 37 states, allowed us to deploy capital with even more intention in 2018. This meant that for every dollar you invested in CNote we were able to deliver significant targeted impact. To illustrate, historically around 4.4% of all small business funding goes to women-owned firms. 2 Meanwhile 43% of CNote’s investment dollars were deployed to women-led businesses, almost 10x the norm. It is radical shifts in capital access like this that will build a more inclusive and robust American economy–which is our overarching mission at CNote.

Finally, on the financial front, starting in January 2019, the rate of return on all CNote accounts will be increasing to 2.75%. This is in furtherance of our goal to prove that impactful investing can be profitable as well.

*Note that pro-forma numbers were updated to final impact numbers on March 6, 2019, after receiving finalized impact data from our CDFI partners. Previously, the above numbers were pro-forma calculations based on Q3 performance and the total capital deployed in Q4.

There’s a saying that goes, “If you bought it, a truck brought it.” That may only be true 73.7% of the time, but either way, there are a lot of truckers out there in the U.S. delivering the things that we use and rely on every day. Over a million, in fact.

Marley Transport & Trucking is one of those trucking companies. Yet, when we interviewed founder Shavon Marley, we found the incredible story behind this company is what makes it stand out from the crowd.

Shavon Marley, Owner & Founder of Marley Trucking

A family-operated business

True to its name, Marley is largely a family-operated business. Shavon Marley started the company. Later, her husband took the primary role as head of operations and dispatch. Her dad was the first driver they hired, bringing decades of experience and industry connections to the table. Her uncle, who had gotten involved in trucking through her dad, is their second driver; and their third and most recent, added due to a higher volume of work, is a friend of a friend.

Marley may be one trucking company out of millions, but it’s more than a business, it’s a family, both literally and figuratively. Needless to say, this small company, which continues to grow, is not only having a significant impact on Shavon’s family but her community as well.

Marley Trucking Team

For Shavon and her husband, it was a dream long in the making. Originally Shavon worked full time in sales, and her husband in cable and satellite installation, a demanding job that required him to work six days a week outdoors. “My husband and I were high school sweethearts also,” she told us. “…We always had this thing where one day we would figure out how to have our own business and set our own schedules, and be able to travel and be able to work from wherever we travel.”

That was the dream. But it was not until the onset of some difficult and unexpected circumstances that Shavon began to take action, turning her dream into a reality.

The above image is of a therapy session occurring in a hyperbaric oxygen chamber. In 2016 Shavon would find herself spending a lot of time in these tanks: she was diagnosed with breast cancer in April of that year.

Others may have balked in the face of such hardships, but Shavon made the most of it. Her treatment allowed her “a lot of time away from work, and also a lot of time to think,” she told us with a laugh. Therapy sessions would last 7 hours each and occur 2-3 times a week — all without the distraction of electronics. She used the time to ruminate at length about the business she and her husband had always wanted to start.

“I’m picking up on inspiration everywhere.” -Shavon Marley

But she didn’t only think. She found herself engaging in conversation with some other patients. “I’m in this tank with all old people — but a really good group of old people.” This included business owners, people experienced in the trucking industry, and even a woman who had started a welding business and could provide advice in thriving in a male-dominated industry. “I’m picking up on inspiration everywhere,” Shavon told us. “So I’m going into this tank with my pen and paper, and I’m getting my questions answered.”

For some specific concerns, however, the people she was close to didn’t have all the resources she needed. “I didn’t really have immediate people within my trust circle I could go to and say, ‘How do I do this? What do I need to know? Does the loan make sense?’…I just didn’t know what to do.” Meanwhile, there was an increasing source of pressure in her ever-growing absence away from work, and her husband’s own job whose hours were long and kept them apart at such a challenging time.

Marley Trucking, a story of teamwork

But her father, a seasoned trucker, always believed in her. “He’d always tell me, ‘You’re a big girl, you’re smart, you can figure it out, you can figure anything out…’ — Okay, well, if I figure it out,” Shavon recounted, “then I solve all these problems.” With some help, she did.

One big part of the equation was assistance from Carolina Small Business.

Figuring it out with Carolina Small Business

When Shavon first connected with Scott Wolford of Carolina Small Business Development Fund, the business she had in mind was a dump truck business. Eventually, this would evolve into the transport and trucking business of today. Needless to say, there was extensive thinking, collaboration, and planning along the way, but Scott’s guidance helped see her through.

Scott found a driven, hardworking client in Shavon. “I think he could tell I’d never written a business plan before,” Shavon recounted. “But I think he picked up on the fact that I’ll research any and everything until I figure it out.” He directed her energies by coaching her on writing the business plan, providing tools and resources, and bringing certain costs and considerations to her attention — “all the things that you really have to kind of put some time into forecasting when you’re starting a business.”

In April of 2018, all of the hard work came to fruition. Shavon received a loan which was able to support her new business and fund insurance for the trucks in her growing enterprise. On April 30, 2018, Marley Transport & Trucking pulled its first load. Since then Marley Trucking has continued to grow and establish itself as a reliable transportation option across North Carolina.

The fast-growing fleet

Conclusion

There were still challenges after launch, such as finding brokers, meeting a high volume of work, and navigating the logistics of intermodal hauling. But Shavon used her trademark grit and research abilities to pull through. Now Marley Trucking has three drivers and does intermodal hauling from the Port of Wilmington.

Recently, Shavon and her husband took a trip to Mexico. Her husband would check his laptop in the mornings, but the afternoons would be devoted to hitting the beach. Working from wherever and whenever they want — their dream had finally come true.

“I don’t think we could’ve done any of that…without the funding,” Shavon told us. “We certainly wouldn’t have been able to grow.”

Learn More

Marley Trucking is based out of Raleigh, NC. If have transport needs in North Carolina, they can be reached at 919-757-5425.

Carolina Small Business fosters economic development in underserved communities through access to capital, business services, and policy research. Since 2010, the non-profit community development financial institution has invested more than $50.7 million through 661 loans to small businesses across North Carolina helping to create or retain more than 2,267 jobs.

CNote has always been committed to delivering tangible social impact while providing competitive financial returns. In 2019, we’re increasing the return on all CNote accounts to 2.75% as we work to prove that investing in a better world can still be profitable.

Impact + Financial Returns

We’ll continue to deliver the same great impact along with assuring that the capital we provide our non-profit partners is affordably priced and will continue to support sustained economic development in communities across America. CNote’s ultimate mission is to help close the wealth gap in America by increasing access to capital for communities that were commonly cut off from traditional funding sources.

Maria Harrington, Owner of Casa de Español, a CNote small business success story

As CNote’s CEO Catherine Berman noted, “For a long time, doing something good with your money wasn’t always the smartest financial decision. We’re challenging that thinking. In 2019, we’re making it even more financially rewarding for our members to invest with their values. If you’ve got extra cash sitting in an account paying you next to nothing, an investment in CNote is a great way to make your money work for you in 2019.”

Next Steps

Existing members don’t have to do anything and will see the increased earnings reflected in their account dashboard for January.

New members can sign up today and enjoy the increased rates starting January as well.

Additionally, CNote members can increase the APY on their accounts up to 3.00% by referring friends and family. You can learn more about the bonus requirements when you log into your secure dashboard.

Note: This is a guest post was authored by Sahil Vakil, CEO of MYRA Wealth. MYRA Wealth provides personal finance services for international and multicultural families in the United States.

What is investment risk, what shape does it take and how does risk affect your personal financial planning? Investment risk is a complex topic, but every investor should have at least a basic grasp of investment risk in order to make wise investment decisions. In this article, we cover the basics around investment risk and explain how and why your approach to investment risk should adjust over time.

Defining investment risk

Investment risk is the likelihood of a financial loss that is caused by an investment. FINRA (The Financial Industry Regulatory Authority) defines investment risk as uncertainty with respect to your investments. It is the probability that upon selling an investment you will receive less than you originally invested, or that the investment return on an asset fails to meet your expectations.

Low risk means a relatively predictable outcome, high risk means that there is a lot of uncertainty about your investment outcome. It is important to understand that investment return and investment risk is directly related.

How much risk you are willing to take is subjective, but you should make an informed decision

Investments with higher returns are also often investments carrying higher risk. The market rewards investors willing to accept a higher probability of loss in return for the opportunity to see a high return. However, some investment risk can be mitigated. By mitigating investment risk you can ensure your portfolio is located on the ‘efficient frontier’. In layman’s terms this means that you get the highest returns for a given level of risk, or are exposed to the minimum of risk for a desired level of investment return.

Types of investment risk

Investment risk can be classified under an almost countless number of categories, but when investing your own money it is worth looking at investment risk from two perspectives.

Systematic (or Non-Diversifiable) risk

Some risks are very difficult to avoid because they are intrinsic to the financial system, or indeed to a specific asset class. It may be difficult to avoid systematic risk, but you can reduce your risk exposure by changing the asset class, or by adjusting your financial planning. Some examples of systematic risk include:

Inflation risk

Locking in a high savings account rate may look attractive, but it can cost you if inflation rises. Though the outlook for inflation is generally stable, investors should consider the risk of rising inflation as inflation can rapidly reduce the value of your money.

Market risk

Entire markets can swing, leaving every asset in an asset class such as stocks nursing heavy losses. The strong downturn in the stock market after the 2008 financial crisis is one example of market risk.

Exchange rate risk

In some countries, exchange rates can rapidly change, devaluing investments held in that currency. The opposite can also happen: if you plan on moving back to your home country from the US you may find your dollar-denominated assets can suddenly lose relative value if your home country’s currency stages a recovery.

Systematic risks cannot be fully avoided but a degree of planning can compensate for systematic risks. Systematic risks are also worth staying ahead of so that you avoid underestimating your overall investment risk.

Unsystematic (or Diversifiable) risk

Some types of investment risk affect individual assets such as specific stocks rather than entire markets. Also known as unsystematic risk, these diversifiable risks can be mitigated by spreading your investments across multiple assets. Diversifiable risk includes:

Regulatory and business risk

Governments can put large companies out of business rapidly, or at least reduce their ability to produce profits. Just think about environmental regulation, for example. Likewise with regards to competition, consumer preferences and technological advances all of which can quickly reduce the prospects of a corporation.

Debt risk

Corporations use debt to finance their activities, and for the most part, this causes no problems. However corporate debt can suddenly spiral out of control, leading to difficulties repaying debt and a contraction in profits or in the worse cases, default, and collapse of the corporation.

Event risk

Unexpected events can impact the ability of a company to maintain growth and profits. Examples include natural disasters, a customer service fiasco or large hacking attacks that lead to financial loss or data loss and the associated bad publicity.

Diversifiable risks are highly unpredictable, but by holding a range of assets (such as a basket of stocks in an ETF) you can reduce the impact of any one stock that suffers large losses. It is worth diversifying not only across companies but also across industries and asset classes.

Adjusting your risk exposure

One of the laws of investing is that returns even out over time. This is known as ‘mean reversion’ – your investment returns will tend to match average returns in the long run. What you lose during one period you will probably later gain over another period – if you invest wisely, of course. In time frames stretching decades chances are you will have the opportunity to make up for losses, so you can take risks.

You must understand and control the risk you take, otherwise you’re just gambling

Deciding how much risk you take on when investing your personal finances depends in part on when you’ll need access to your money. If you have no looming large expenses such as a mortgage deposit, children’s college fees or indeed retirement you can take bigger risks with your investment funds.

On the flipside, if you will need your funds in the near or medium term you need to lower your risk exposure as you may not have enough time to make up any losses suffered by your investment portfolio.

Investing with your life goals in mind is called ‘goal-based investing’, in other words you focus on attaining specific financial goals such as saving for your children’s school fees, rather than investment goals such as maximizing returns or beating market performance.

Other risks relevant to personal investment

Adjusting a personal investment portfolio to adequately take account of all risk factors is difficult, compounded by the risk factors faced by individuals. For one, your investment horizon can be abruptly shortened due to an unforeseen event, such as a loss of employment or a medical condition. This so-called ‘horizon risk’ matters because it can force you to endure big losses on investments you were not expecting to sell.

Personal investors also face another, often ignored risk: that of ‘longevity risk’. What happens if you outlive your savings? Or indeed, if you pass away before you can fully utilize your savings, in the absence of an heir?

Getting advice on personal investment risk

It should be clear by now that the risks faced by personal investors are varied and complex. On top of that, you need to adjust your response to investment risk over time. Juggling this intricate set of rules and facts can be a challenge and expats (including international families) have additional factors that they need to take into account.

Qualified, experienced personal financial advisors should help you navigate the risky waters. Typically financial advisors will try to understand your risk profile by asking you a set of questions or having you complete a survey in order to craft a portfolio that meets your needs and goals, on a risk-adjusted basis. This objective process determines your personal tolerance to risk, mapping out an investment strategy including the assets that match your risk preference. For example, Myra Wealth utilizes Prospect Theory, a Nobel Prize-winning model of behavioral economics, to conduct an individualized risk analysis for each of their clients to set transparent goals and expectations for their investments.

As much as you should consider professional advice for investment, a basic awareness of how investment risk works can help you gauge the quality of the advice you are receiving.

If you’ve tuned into financial news at all lately, no doubt you’ve heard that the United States Federal Reserve has continued to slowly but steadily “hike” the interest rate. In September 2018, the third of four planned increases on the year resulted in an effective interest rate in the range of 2.00%-2.25%, the highest since immediately prior to the financial crisis of 2008.

But what does the Federal Reserve actually do and how does it control interest rates? And, most importantly, what do higher interest rates mean for you?

The Federal Reserve

The United States Federal Reserve System, colloquially referred to as “the Fed,” is the central banking system of the United States. It is a quasi-private entity that operates within the federal government and is comprised of twelve regional Federal Reserve Banks, a board of governors, the Federal Open Market Committee (FOMC), and thousands of member banks on the state level.

Official Seal of The Federal Reserve

The Fed’s key roles are defined in its so-called dual mandate, which stresses the promotion of full employment and price stabilization as the major objectives of the Fed’s monetary policy. The responsibilities of the Fed have grown in the century-plus since its 1913 inception to include the regulation of banking institutions and facilitating foreign exchange of payments. To that end, the Fed engages in oversight and control over the entire financial system in an attempt to pursue its policy objectives.

The manipulation of interest rates is a principal tool by which the Fed attempts to control macroeconomic indicators such as unemployment and inflation. Fed actions in monetary policy have significant and far-reaching impacts, affecting everything from the cost of paying off credit card debt to the prices of goods on store shelves. Therefore, it is important to understand why and how the Fed controls the interest rate as well as the ultimate effects of their policies.

The Importance of Interest Rates

The interest rate represents the time value of money. Since humans tend to value present goods higher than future goods, lenders must be paid back more in the future in order to part with money today. The additional sum of money that the borrower later pays back to the lender is some fraction of the principle of the loan, which in percentage terms is the interest rate.

Jerome Powell, Chair of the Federal Reserve

Here’s a simple mathematical example to drive the point home. Imagine you borrow $1,000 from a bank today with the promise to pay the sum back one year later at a 10% annual interest rate. In one year, you will not only return the $1,000 you initially borrowed, but an additional $100 to compensate the bank for the value of time between receiving the cash and paying it back. While you receive $1,000, you pay back $1,100 at the end of the loan period to compensate the bank for the time value of the money you borrowed for the duration of one year.

Interest rates are thus an essential indicator of the total savings in the economy. Absent intervention from a central bank, less savings means more demand for whatever credit is available, which pushes the interest rate higher. On the other hand, more savings means that credit is more plentiful, resulting in a lower interest rate.

In that way, interests rates are the key signal for business owners and entrepreneurs to determine if pursuing a given economic project is feasible given the cost of borrowing. If credit is expensive at higher interest rates, those pursuing stable, shorter-term projects are more likely to afford the high cost of credit than those with riskier long-term projects in mind. In the event that interest rates are low from a genuinely high pool of real savings, entrepreneurs who otherwise could not have been able to afford the cost of borrowing might now be able to acquire the capital required to kick off their projects.

The Fed and Interest Rates

So why does the Fed bother with the interest rate in the first place? The answer lies in the aforementioned dual mandate. The Fed believes that it can use the interest rate as a lever to pursue its policy objectives of both low unemployment and low inflation.